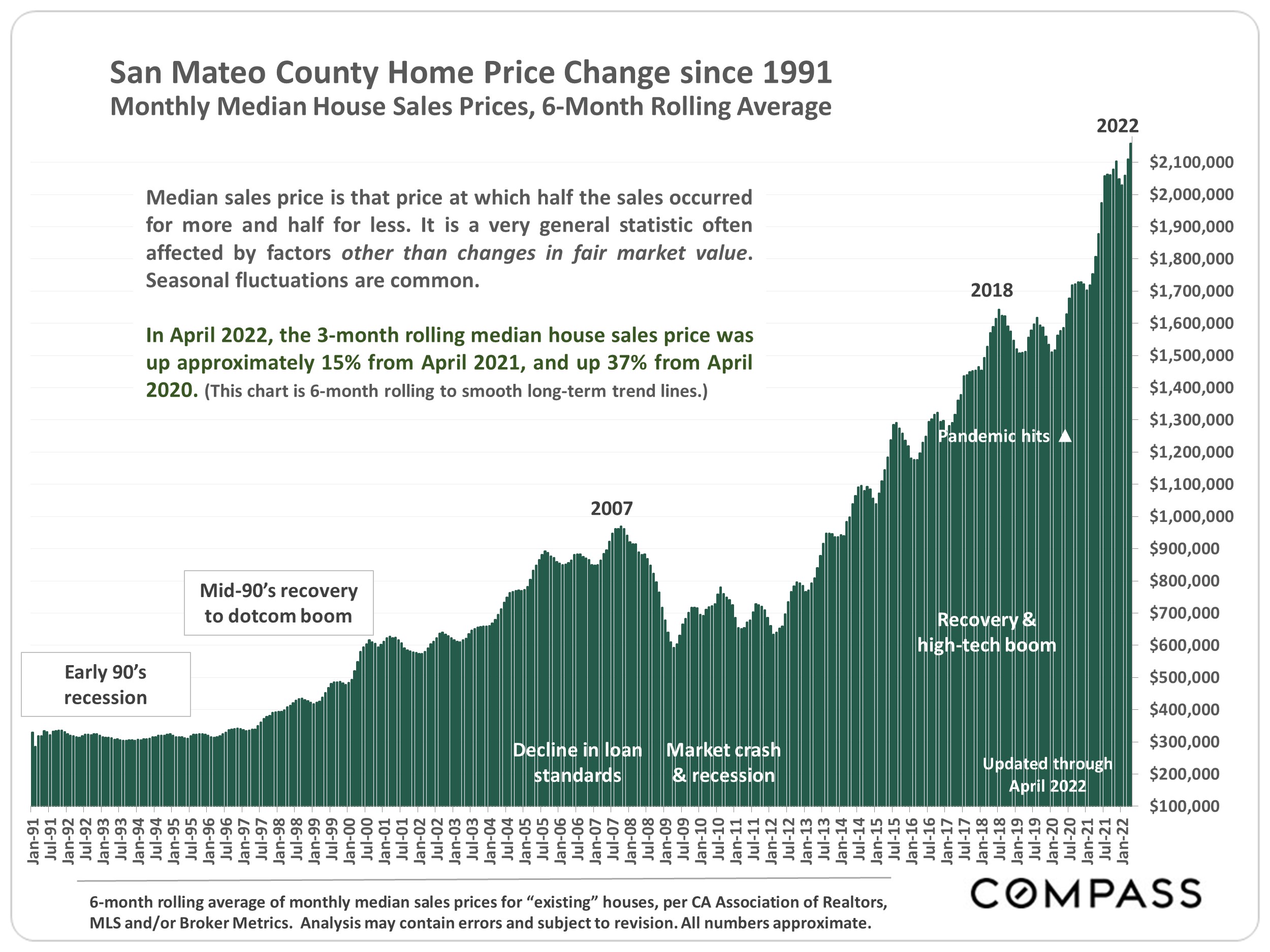

After the Early 1990’s Recession: Recovery & Dotcom Boom

From 1990 – following the late 1980’s stock market peak, the S&L/junk bond crisis, and 1989 earthquake – through the recession to the mid-1990’s, Bay Area real estate markets generally remained weak, with prices typically declining 5% to 11% within the period. In the middle of the decade, markets began to recover, with home prices subsequently accelerating rapidly during the dotcom boom.

Once the dotcom boom got going, San Francisco and Santa Clara Counties, the centers of the phenomenon, saw the highest appreciation rates. Adjacent counties saw lower, though still substantial increases, with rates in the next circle of counties stepping down further. The Bay Area generally saw appreciation percentages peak dramatically in year 2000, the height of the dotcom bubble. National home-price appreciation during this period was considerably lower than in the Bay Area.

The chart following this page illustrates these trends.

When dotcom hysteria collapsed and the Nasdaq crashed, only the inner Bay Area Counties – SF and Santa Clara, and those adjacent to them – saw significant (though relatively short-lived) median price declines, while outer counties were generally unaffected. According to the Case-Shiller Home Price Index for the multi-county San Francisco Metro Area, the dotcom collapse affected high-price home markets the most, low-priced homes not at all, and the mid-price segment somewhere in between. More affluent homeowners – also tending to be concentrated in inner Bay Area Counties – were most affected. This is a relatively consistent trend historically: Higher-price home markets are much more sensitive to negative changes or simply uncertainty in financial markets.

|

The Subprime Bubble

The subprime bubble and crash was an anomalous situation caused by predatory lending practices, the abandonment of underwriting standards, dishonest financial engineering on Wall Street, and irrational exuberance in financial markets. This led millions of borrowers to take on purchase and refinance loans unaffordable from the moment deceptive “teaser rates” expired. (We believe giving vast numbers of loans to unqualified borrowers, then using these junk loans to create the “A” rated securities which almost caused a worldwide great depression to be anomalous. Perhaps we’re being naive.) When the music stopped, a crash in financial markets, and a flood of foreclosure and short sales created a fast, deep spiral of home-price declines.

The crisis resulted in large numbers of homes being sold for well below fair market value, which distorts the meaningfulness of median sales price changes during this period. Enormous median price declines occurred, sometimes exceeding 45% (see following charts). “Distressed” homes sold at unnaturally depressed prices, as these transactions often entailed desperate sellers; more hassle, time, uncertainty and risk for buyers; and the homes were often in significantly poorer condition than the norm.

Part of the definition for “fair market value” is that the seller is not in a situation of being forced to sell quickly. Sellers of foreclosures & short sales – whether homeowners or banks – were usually in urgent distress: This undermined fair market value and provided excellent deals for buyers and hedge funds.

Less expensive, less affluent, less financially sophisticated markets were hammered worst by predatory lending and subprime loans, seeing the largest bubbles and crashes. The most expensive/affluent markets saw much smaller bubbles, and smaller, but still significant price declines, probably caused more by the financial markets crash than by a relatively low number of distressed-home sales. Effects varied greatly by community within counties, generally correlating to cost/affluence: Prices in less expensive markets often dropped twice as much as in more affluent communities within the same county.

The next 2 charts look at this period first by price segment, then at the size of subprime-bubble price declines by county.

|

Recovery from the Subprime/Financial Markets Crash

Generally speaking, Bay Area real estate markets began their sustained recovery from the effects of the subprime-loan bubble/financial market crash/distressed-property crisis in 2012. An unusual mix of factors subsequently came into play behind the highest rates of appreciation:

1) Whether the county was one of the three at the very heart of the high-tech, venture capital/start-up and IPO booms: San Francisco, San Mateo & Santa Clara

2) Whether the county was adjacent to (or across a bridge from) the 3 central counties, but offered significantly more affordable home prices: Alameda was the prime example

3) Whether the county was rebounding from a distinctly outsized crash following the subprime bubble, when their overall markets were utterly dominated by foreclosure & short sales: For example, Contra Costa (especially north county markets); Napa; Alameda (especially Oakland); Solano; Sonoma

Marin County is an interesting case during this period from the 2012 recovery to the pandemic striking: An affluent, highly desirable market, it saw substantial appreciation, but 1) was not one of the counties at the very heart of the high-tech boom, 2) though close to San Francisco, its housing wasn’t enormously more affordable (as was the case in Alameda County), and 3) Marin was one of the very affluent counties least affected by subprime loans. Thus, its appreciation rate during this period lagged other Bay Area Counties, which were boosted by 1 or more of the 3 factors listed above. But Marin’s appreciation dynamics would change dramatically with the onset of the pandemic.

The next chart illustrates approximate home-price appreciation rates from 2012 to Spring 2020.

Important notes and caveats regarding the context and methodology of this report are detailed on the last page.

|

The Pandemic Market

Since the pandemic struck in Spring 2020, Bay Area real estate markets have been affected by many diverse and shifting factors, some of them unique to the period. These include population-density and contagion issues; shelter-in-place and its varying effects on urban, suburban and rural environments; work-from-home upending the relationship between home location and workplace; trillions of dollars of free money issuing from state and federal governments; the historic plunge in interest rates (through 2021); a renewed, pandemic boom in high-tech; an astounding surge in stock markets and household wealth (through 2021); the rollout of vaccines; infection rate surges; as well as other ecological, political, economic and social factors (fires, taxes, unemployment, family care, etc.).

These factors, as they applied in their various combinations to millions of households, prompted big changes in county-to-county migration; the comparative appeal of urban, suburban and rural locations; the desirability of different property types (houses, condos, apartments) and amenities (pools; yards, gardens and decks; home and lot size); a heightened attention to housing affordability between regions (now that many could work from anywhere); and surging luxury home and second-home sales. Waterfront homes, in particular, became highly sought after. Some changes have ebbed and flowed over the period.

All this brought about striking changes in market dynamics and appreciation rates. Some of the larger trends were significant population movements from expensive, urban markets to suburban and rural areas. In the immediate aftermath of the pandemic, this migration precipitated a distinct weakening of rental and condo markets (which subsequently saw recoveries in 2021/2022). Some counties saw disproportionate increases in sales of larger, more expensive homes, a big factor in boosting median sales prices: This affects apples-to-apples comparisons of appreciation rates between counties.

The following chart illustrates approximate home-price appreciation rates from Spring 2020 to Spring 2022, i.e. during the period since the pandemic first hit. Note: In early 2022, major macroeconomic changes – such as rising interest rates and volatile stock markets – hit the economy, but through April 2022, median home prices continued to increase.

|

Early 2022: Median Home Prices Still Rising, But Effects of Major Macroeconomic Changes Pending

Bay Area home markets through April 2022 generally continued to see home-price gains to new peaks, and statistics based on closed sales during this period still reflect intense demand competing for an inadequate supply of homes for sale. (Note that supply and demand dynamics, and price appreciation rates, between house and condo markets typically diverged substantially over the past 2 year.) However, interest rates soared 64% in the first 4 months of the year, and stock markets continue to experience high volatility with significant declines occurring during the period. The effects of these changes have just begun filtering through to the market – as seen in declines in open house attendance and the number of offers received by new listings, changes in plans by some buyers and sellers, and drops in the number of listings going into contract – but have not yet shown up in closed-sales statistics. (Closed sales are lagging market indicators, reflecting new listings coming on market, interest rates, and offers being accepted 4 to 8+ weeks earlier.)

What exact effects these recent economic changes may have on markets and home prices are unknown. It is extremely difficult, if not impossible, to predict the effects of the almost infinite variety of economic, political, demographic and environmental factors – arising, changing and interacting locally, nationally and internationally – that can impact financial and real estate markets.

A more detailed explanation of context, methodology and caveats can be found at the end of this report.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results. |