Across the Bay Area, markets have continued to slow and cool. As illustrated in this report, dramatic changes in demand, inventory, overbidding, price reductions, and year-over-year appreciation rates have usually occurred. Buying and selling continues: Over 5200 home sales were reported to MLS from Napa County to Monterey in July 2022 – many of them selling quickly for over asking price – but that number was down 38% from last year. Median home price appreciation rates in the Bay Area have seen steep declines from those in 2021/early 2022. All these changes vary in degree by location and market segment, but the direction of these shifts is near universal.

This report will review year-over-year changes in prices, and in supply and demand, reflecting the significant adjustments from the heated (often overheated) conditions recently the norm, but also look at longer-term trends to provide greater historical context. There is also a comparison of home prices within the local market, as well as across the Bay Area.

As of early August, the average, weekly mortgage rate for a 30-year fixed rate loan fell below 5% for the first time since April, and stock markets have seen large rebounds since early July – but these and other indicators have been subject to sudden and often dramatic volatility, and their future directions can’t be taken for granted. Within this report is a link to a review of many of the macroeconomic factors at play.

According to some agents, buyer interest has begun to rekindle with the decline in competition, increase in inventory, and economic changes mentioned above, but if this is part of a broader recovery in demand, it has not yet shown up in the statistics – which are lagging indicators of what’s occurring on the ground right now. Monthly data can be volatile, fluctuating according to a wide variety of factors, including market seasonality. Longer-term trends are more meaningful than short-term fluctuations.

Mid-late summer is typically a slower period compared to the big, spring selling season. Autumn sometimes sees a significant spike in new listings and sales prior to the big mid-winter slowdown.

Our reports are not intended to convince you regarding a course of action or to predict the future, but to provide, to the best of our ability, straightforward information and good-faith analysis to assist you in making your own informed decisions. Statistics should be considered very general indicators, and all numbers should be considered approximate. How they apply to any particular property is unknown without a specific comparative market analysis.

Source: Compass

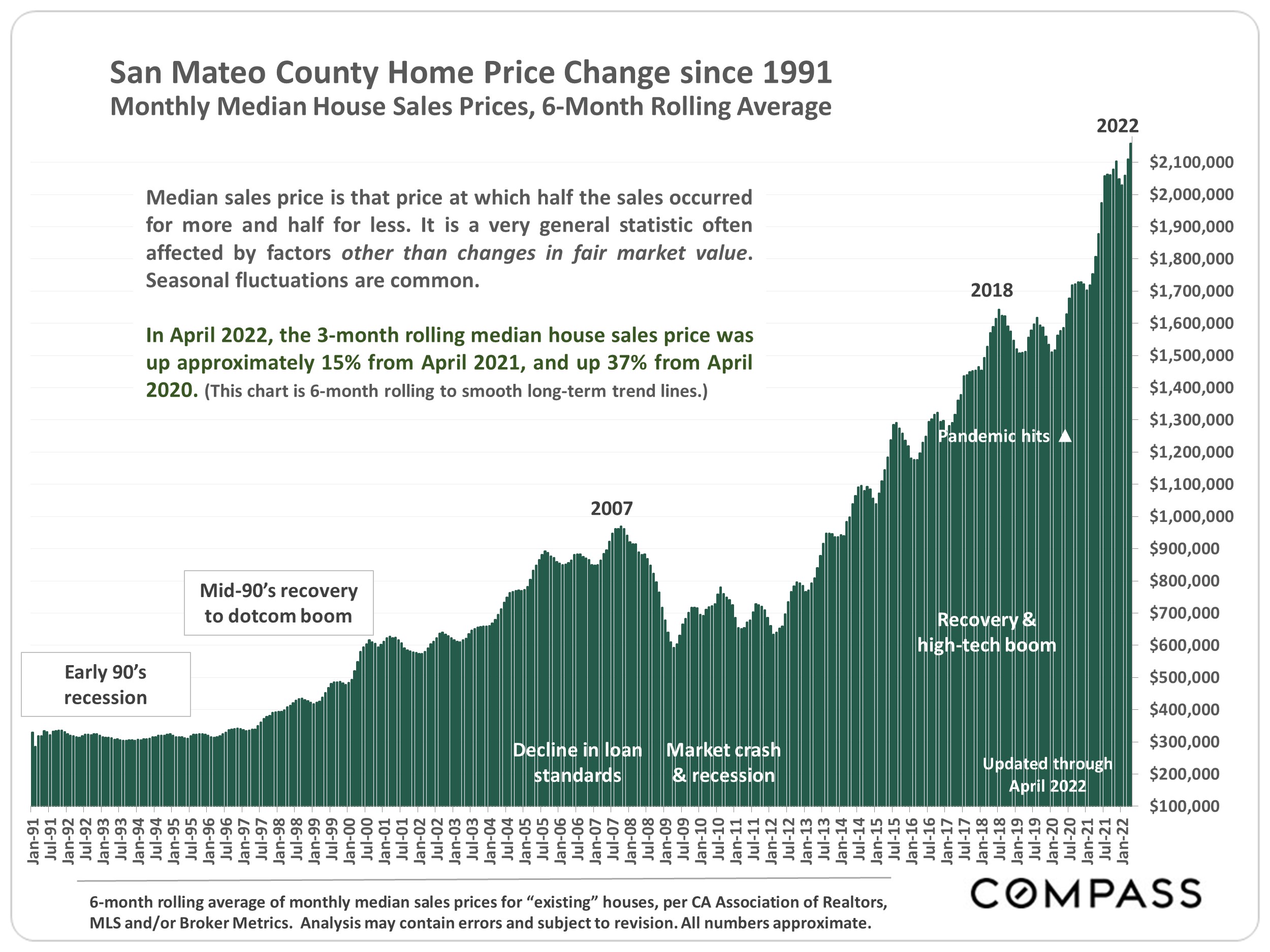

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.