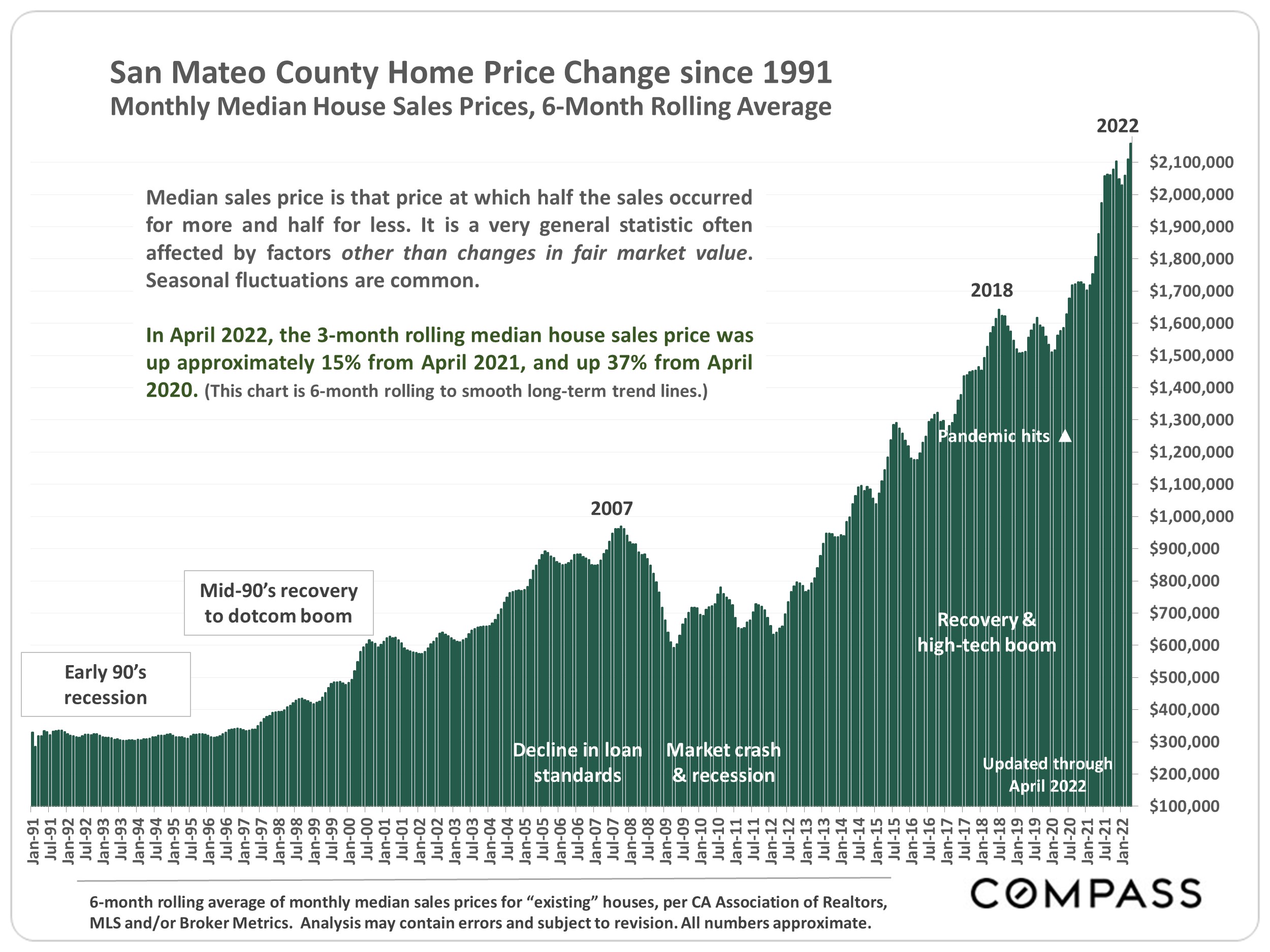

Clear Indications of Changing Market Dynamics

Sales are declining, and the number of active listings and price reductions are increasing. But the homes that are selling are still, on average, selling very quickly for well over asking: In May 2022, 86% of sales closed for over list price, at an average overbid of 11%. Median sales prices and year-over-year appreciation rates remain very high. When an overheated market cools, the change is typically gradual (absent a disaster event) and does not mean the market is weak by any normal standard. As an analogy, if traffic is going 120 miles per hour and drops to 75, it feels a lot slower, but cannot reasonably be described as slow. After 2 years of scorching demand, it may be difficult to remember what a more normal market feels like, but people will continue to have excellent personal and financial reasons to buy and sell homes.

As of late spring, across the Bay Area, less expensive home sales have generally been considerably impacted by rising interest rates. Sales of higher-priced homes have held up much better, but cooling demand is beginning to show up in pending-sale data. (Affluent buyers tend to be more affected by financial markets, which became very volatile in May.) Market changes are often very uneven in the early months of a transition, with one home selling in days at 20% over the list price, while next door, the seller has to reduce their price to get an offer. As markets cool, buyers become more discriminating; negative conditions previously ignored are noticed; more negotiation occurs; multiple offers and overbidding decline. Listings that are well prepared, show well, and are priced right will have an increasing advantage.

The homes that are not selling quickly won’t affect overbid and days-on-market statistics until future months. The high appreciation rates of the last 2 years will almost certainly start to decline (which is not the same thing as an imminent decline in prices). After peaking in spring, activity in the county typically gradually slows through summer and fall prior to the mid-winter slowdown. Sometimes, autumn sees a small, short spike up. These are common seasonal dynamics, though other factors can come into play.

This report will look at recent, year-over-year changes in inventory and demand, while also reviewing longer-term trends for more context. Included is a link to a report reviewing city/town submarkets.

National Housing Market Reports

Being the center of high-tech industry and other unique local factors deeply affect Bay Area real estate, but the differences between local and national trends are generally more of degree than direction. General economic conditions and broad market trends up or down typically run on similar tracks across the U.S.

“Active inventory continued to grow, rising 11% above one year ago. In a few short weeks, we’ve observed a significant turnaround in the number of homes available for sale, going from essentially flat at the beginning of May to +11% in the last week of the month.” Realtor.com Report, June 6, 2022

“Pending contracts… better reflect the timelier impact from higher mortgage rates than do closings,” said Lawrence Yun, NAR’s chief economist. “The latest contract signings [in April] mark six consecutive months of declines and are at the slowest pace in nearly a decade’ With mortgage rates rising, Yun forecasts existing-home sales to wane by 9% in 2022 and home price appreciation to moderate to 5% by year’s end.” National Association of Realtors, May 26, 2022

“Mortgage rates continued to inch downward this week but are still significantly higher than last year, affecting affordability and purchase demand. Heading into the summer, the potential homebuyer pool has shrunk, supply is on the rise and the housing market is normalizing.” FHLMC (Freddie Mac), June 2, 2022

“Mortgage applications decreased to the lowest level since December 2018, as the purchase market continues to struggle with supply and affordability challenges… applications last week were 14 percent lower than last year, with more activity in the larger loan sizes. Demand is (still] high at the upper end of the market, (where] supply and affordability challenges are not as detrimental… as they are to first-time buyers.” Joel Kan, Mortgage Bankers Association, June 1, 2022

Source: Compass

|

|